What if…?

Peek into 'no cash' simulations

Theoretically, a discerning allocator should be ok with elevated volatility if risk-adjusted returns are also superior. Discerning allocators invest with long time horizons, and have the capacity to withstand even significant temporary drawdowns. However, there is an undeniable scarcity of such allocators in India, which coupled with inherently poor short-term price discovery, drives an allocation mindset that bizarrely eschews downside volatility despite often unrealistic return expectations. Their advisors are occasionally neither discerning enough nor fiduciary enough.

Investment strategies should be designed to force their way either on or close to efficient frontiers of discerning allocators. Differentials in underlying exposures, and favorable asymmetry within other attributes are critical in getting there.

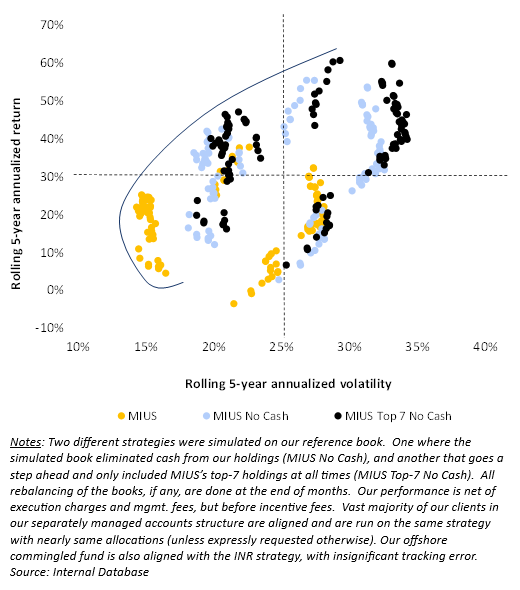

In the attached exhibit, we simulated an alternative frontier of our own strategy. Historical 5-year rolling returns (since strategy’s inception) of 3 different books were plotted – 1. The reference book itself (in orange), 2. Simulated book that didn’t retain any cash at any point (in blue), and 3. Simulated book that didn’t retain any cash at any point AND only held our top-7 positions (in black).

While all books make a compelling case to get on most efficient frontiers, it is worth questioning if elevated volatility in such simulations was worth it. If (!!) an allocator has the patience to invest over long timeframes, it is hard to argue against a full allocation into strategy’s highest conviction (defined here as top-7 positions by weight) holdings i.e. the third choice referenced above - In majority (not all!) of the 5-year periods, this simulated strategy delivered the highest Information Ratios, with the strategy compounding at nearly 33% over decade and a half, vs. 17% for the Minerva India Under-served strategy and 12% for BSE Smallcap. That said, as is evident (refer to the black dots on the right of the exhibit), there are multiple 5-year periods when this simulated ‘Top-7 No Cash’ strategy would have had annualized volatility of >30%. Clearly, this would have been a stiff test of patience, which is often in short supply in India.

As always, superior risk-adjusted measures by themselves do not necessarily align with an institutional allocator’s actuarial targets and investment program goals.

For questions on simulations, please reach out to Devchandra Ramani or Deepak Gaur.

DISCLAIMER: The information, opinions, estimates and projections contained in this note were prepared by managers of Minerva India Under-served and constitute its current judgment as of the date of this note. The information contained herein is believed to be reliable and has been obtained from sources believed to be reliable, but we make no representation or warranty, either expressed or implied, as to the accuracy, completeness or reliability of such information. We do not undertake, and have no duty, to advise you as to any information that comes to our attention after the date of this note or any changes in its opinion, estimates or projections. Prices and availability of securities are also subject to change without notice. This is not a prospectus and does not constitute investment advice or an offer or solicitation to buy or sell any designated investments discussed herein. Neither Minerva Asset Advisors, nor its officers, directors, agents, or employees make any warranty, express or implied, as to the suitability of any fund as an investment or of any kind whatsoever, or assumes any responsibility for, and none of these parties shall be liable for, any losses, damages, costs, or expenses, of any kind or description, arising out of this note or your investment in any fund. You understand that you are solely responsible for reviewing any fund, its offering and any statements made by a fund or its manager and for performing such due diligence as you may deem appropriate, including consulting your own legal and tax advisers.